Can the Nasdaq rally like its 2009?

Your Daily KnowHow

The Daily KnowHow is free and we want to keep it that way. If you find our work valuable, please subscribe and share. This is real analysis by real analysts. Enjoy!

In today’s KnowHow…

Can the Nasdaq rally like its 2009?

So that was a big inflation number…

Musk’s U-turn is at odds with Cathie Wood’s views…

Alphawave slumps 19% on debut as London IPO market stutters again

What happened overnight…

It may be a new day, but it’s the same story with inflationary worries once again driving the markets. Global stocks have fallen to a six-week low and the MSCI World hit its longest selloff since September, finishing down yesterday for the fourth day in a row. In the single stock space, BT and Burberry are making the headlines in Europe with the former trading down 5% and the latter down 8%, off the back of poor results. Over to the US and all eyes will be on Alibaba who are due to report this morning with the shares down 5% YTD having been hit by both the Chinese regulatory issues and the growth rotation. Finally, it wouldn’t be a daily without an Elon Musk headline and he once again came up trumps suggesting that Tesla will stop using Bitcoin. Now, below $50,000 overnight (more below).

Chart of the Day

Exhausted from all the inflation and rotation chat? We certainly are. So, we’re going a little left field today with this chart that caught our eye.

Analysis

Can the Nasdaq rally like its 2009?

Another question, this time from Martin N, following our analysis of the post-GFC rotation in 2009. During that time, the Nasdaq doubled quickly from its lows and out-performed the Dow Jones soon after despite rising rates. As a starting point, let’s look at the relative composition of the Nasdaq 100 in 2009 vs now. Below from Nasdaq Intelligence. This is largely why we also looked at S&P Growth vs Value in our rotation models.

You’ll see that the make up was very different. A much larger skew towards telecoms as opposed to the large scale growth of Big Tech that we have today. And, unlike the financial crisis where the selling and earnings impact was largely indiscriminate, during the pandemic, a large number of Nasdaq constituents have been crisis winners. In fact, their earnings have accelerated through the pandemic.

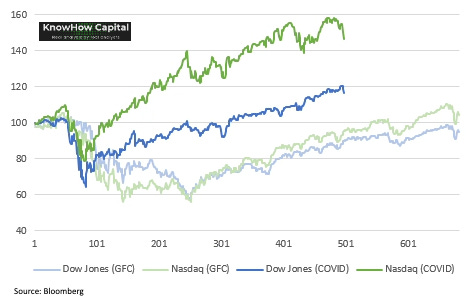

Below, shows the performance of Nasdaq and Dow pre and post GFC and COVID. You’ll see we are starting off from a very different base today versus 2009 where the Nasdaq initially was playing catch-up at this point.

But, the earnings trajectory is only part of the story. When carrying out any crisis analysis, comparing pre vs. post crisis gives the best gauge of how the market is viewing the world. The Nasdaq now trades at a 30% premium to pre-crisis, again, a very different situation to GFC.

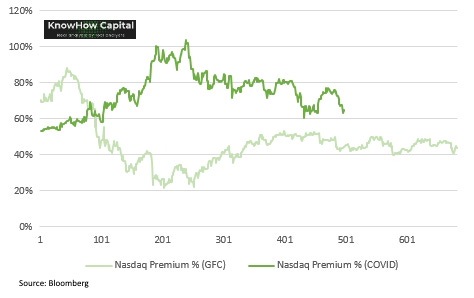

Further, the premium of the Nasdaq vs. Dow on an EV/Sales basis has expanded considerably through the pandemic. During the GFC, the premium actually fell dramatically. Even after valuations went up, the premium remained well below pre-crisis levels. Of course, Apple infamously changed that almost two years later, becoming 20% of the index. That valuation dynamic caps any 2009 like rally in the Nasdaq.

So, why can we still use the GFC playbook for our rotation models? Well, the above chart is the key one. Relative valuations have come back considerably and the Nasdaq premium is now only marginally above pre-crisis levels. We think that is justified. That is not the case for high growth yet but certainly is for Big Tech.

What we’re reading

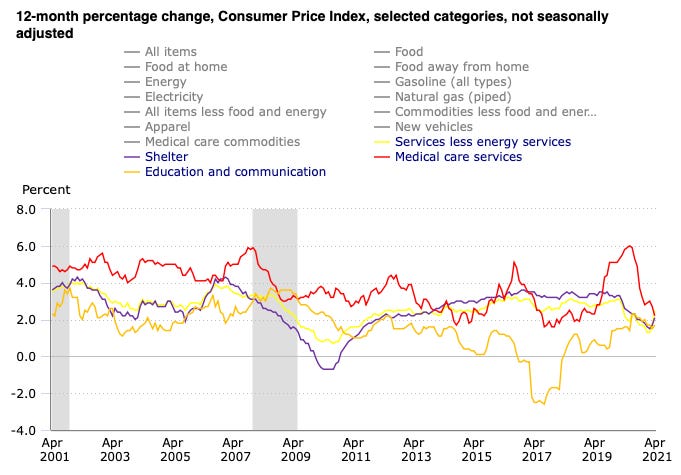

So that was a big inflation number…

Yesterday we flagged the upcoming US inflation data as a “meaningless data point riddled with base effects” that would get bulls and bears unnecessarily excited. Hmmm… may have gone a bit hard on that one. It turned out to be a pretty big number and it’s fair to say that even the Fed probably sat up and took notice. But, does it change the bigger picture? We still don’t think so. Yields spiked and that probably encourages some further outflows from equities but, as the below chart suggests, the areas of inflation that the Fed will care on are still ok. Plus, the real driver of that print, commodities, will respond to supply driven by higher prices. What we care most about is what the data looks like in Q3 and how wage inflation comes through. That will dictate how the Fed responds.

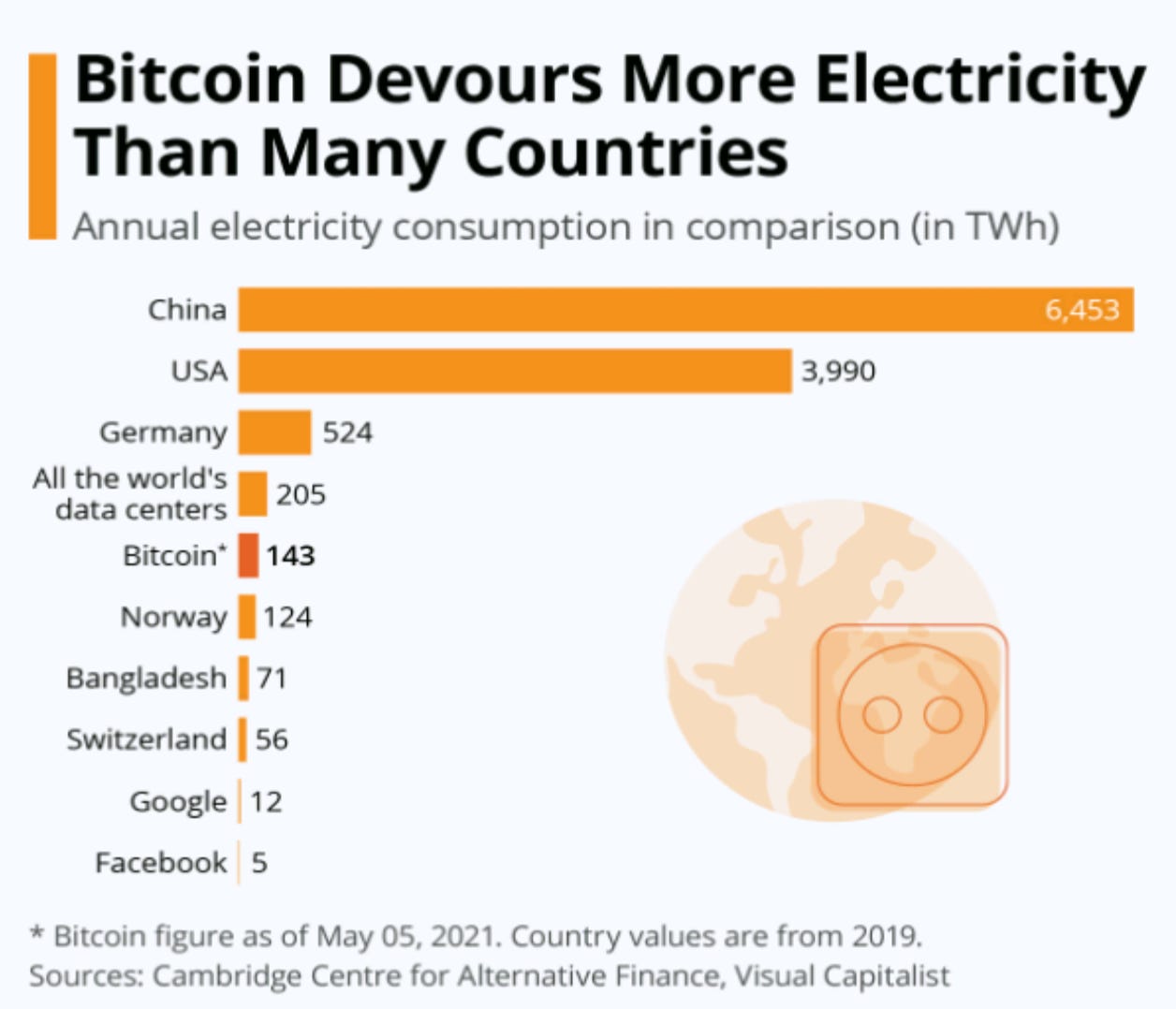

Musk’s U-turn is at odds with Cathie Wood’s views…

While we all saw the headlines and the subsequent fall-out for Bitcoin (more here), the ESG angle is really interesting for us and a debate that will likely rage on for a while. It is no secret that Musk has faced sharp rebukes over Tesla’s support for bitcoin, including from ESG investors who prioritise environmental, social and governance issues. However, this comes just three weeks after he appeared to endorse research from Cathie Wood’s Ark Investment Management LLC asserting that Bitcoin mining could end up being good for the planet by incentivizing renewable power. On a side note it was also interesting to see Ether, the second most valuable cryptocurrency, has said it was moving to an alternative method known as “proof of stake”, which does not depend on the same energy-hungry method. As we said, the debate will likely continue for a while but the below chart does certainly suggest something needs to change…

Alphawave slumps 19% on debut as London IPO market stutters again

Given the sheer volume of paper that came to market in Europe this week (Monday evening saw over €4bn in Europe) and the current risk appetite, the IPO of the Canadian semiconductor company Alphawave in London has been viewed as a bellwether for live risk appetite in Europe. As a result, while this is by no means the first IPO to drop 20% on its first day of trading recently (Deliveroo fell by 30%), it is another example of the risk-off nature of a market that had got ahead of itself, especially in the tech space. As a reminder, we wrote a few weeks ago that our sentiment indicators were suggesting a pullback was likely and with inflation worries only increasing post yesterday’s print, does nothing to allay any investor fears.

What is perhaps more worrying is the fact that Alphawave had already compromised on pricing during the marketing process for the initial public offering (IPO), selling shares worth 856 million pounds near the middle of a previously announced price range at 410 pence, giving a valuation of 3.1 billion pounds. We find the ECM market a great tracker of live risk sentiment and the performance today does very little to suggest the current themes playing out in the market will stop.