Copper, gold or rates… which is telling the truth?

Your Daily KnowHow

The Daily KnowHow is free and we want to keep it that way. If you find our work valuable, please subscribe and share. This is real analysis by real analysts. Enjoy!

In today’s KnowHow…

Copper, gold or rates… which is telling the truth?

IEA Net Zero 2050 Report

Short SPACs with this New ETF

Oxford/AstraZeneca booster works well

100 stocks most exposed to a retail unwind

Our note and stock screen is now out for paying subscribers only. You can access is here.

We think this screen is important from a risk management perspective as retail activity remains concentrated in certain stocks and the risk of an unwind post re-opening remains high. We’ve considered three factors to build the database: liquidity, option activity and noise. If you’re a subscriber, feel free to send us your portfolio or key stocks and we’ll evaluate your retail exposure for you.

What happened overnight…

It seems like inflation worries are once again weighing on markets with US futures dropping overnight, following the moves lower in Europe. Copper is also trading off as the ECB joined a growing chorus of names warning of ‘remarkable exuberance’ in markets which hasn’t helped the situation (see some of our thoughts below). In terms of data released, while the market is eagerly awaiting the FOMC minutes, we think it should be a bit of a non-event today as the minutes are from a meeting held before the release of weaker-than-expected jobs and stronger-than-expected inflation data. So, take these with a pinch of salt. Finally, yields on the 10-year rose while the dollar held near its lowest level this year.

Chart of the Day

This one comes from Bloomberg’s Francine Lacqua and it’s another crypto/Elon fest. Looks like the Elon premium has now left bitcoin… but does it mean cryptoland can now find a floor? Hold on… I thought Elon leaving was good for crypto. Pomp?

Analysis

Copper, gold or rates… which is telling the truth?

This was raised by Michaela Arouet on Twitter yesterday so credit goes to her for kicking the KnowHow team into over-drive. The question goes something like this… if you look at the below chart of the copper-gold ratio vs US 10yr real rates, there has been a dislocation between copper, gold and real rates. So, is copper too high, gold too cheap or real rates too low?

Why does the relationship matter?

Let’s start with why the relationship has held historically. Simplistically, copper is an industrial metal driven by GDP growth. Gold is obviously a safe haven metal. A rising copper to gold ratio indicates improving industrial activity and should be in tandem with a pick-up in economic outlook and real rates expectations. But, there are a number of factors at play today that are potentially skewing that relationship:

we are seeing a sharp post-recession re-stocking cycle for industrial and agricultural commodities. That means commodity inventories are tight and supply chains are under pressure. But, supply responds to price and these effects should ease.

gold has been facing competition from bitcoin as a potential safe haven /US dollar debasement asset. We have been doing some work on this and believe a decent part of institutional demand has gone into bitcoin as opposed to gold in recent months.

the Fed is buying treasuries whilst other central banks are enacting yield curve control. That dynamic is clearly keeping rates artificially low.

Gold is cheap

So, what’s the right answer? In our view, the Fed is going nowhere anytime soon which means real rates remain anchored. Meanwhile, the recent volatility in bitcoin should then also support gold flows. That is already starting to happen. i.e. Gold is too cheap. But, it doesn’t stop there…

But, is copper in a speculation bubble?

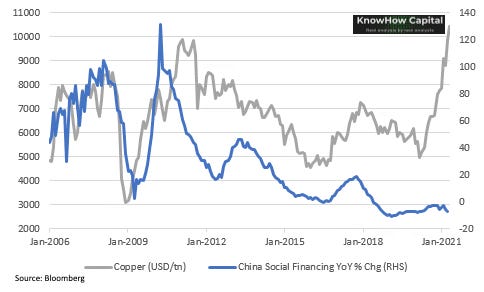

If you have been a copper analyst over the past few years, two of your trading/tactical analytical tools have been CFTC Futures positioning and China Social Financing growth in shadow banking. China monetary growth has tended to drive speculative activity in copper, particularly through shadow banking i.e. outside traditional lenders.

Below is the CFTC non-commercial futures positioning, a good proxy for speculative flows. It is high, and as high as it has ever been since the CFTC began publishing the data.

Now, this chart below is a longer-dated relationship showing the growth in China’s shadow banking. It has tended to be a good indicator of speculative flows in China. But, that relationship has broken down as the Chinese government looks to clamp down on shadow banking.

When you put the two together, it suggests to us that speculative activity is being driven less by Chinese monetary flows with local authorities looking to limit price growth in key commodities. Those flows also tend to be fickle and volatile. Instead, we think the current elevated futures positioning is driven more by stickier institutional flows. And, there is potentially very good reason for that as the CRU has been pointing out.

What we’re reading

IEA Net Zero 2050 Report

If you read one thing over the next few days then this should be it. We plan to follow-up on this with some analysis on the spaces we like so keep your eyes peeled. Yesterday the International Energy Agency (IEA) published their Net Zero 2050 Report. The aim of the report was to outline the essential conditions for the global energy sector to reach net-zero CO2 emissions by 2050. It presents the "most technically feasible, cost-effective and socially acceptable pathway" for achieving this. In terms of their key conclusions, exploitation and development of new oil and gas fields must stop this year and no new coal-fired power stations can be built. On top of this, the IEA suggested that no new fossil-fuel cars to be sold beyond 2035, and for global investment in energy to more than double from $2tn (£1.42tn) a year to $5tn (£3.54tn). The result would not be an economic burden, as some have claimed, but a net benefit to the economy in their opinion. The below chart summarises the path to net zero very well so it’s worth spending some time on it.

Short SPACs with this New ETF

We have spoken a length in the past about the risks posing the SPACs and since February the IPOX SPAC Index, an index that is able to get an overview of pre-deal SPACs, is down over 25%. The issue for many has been how you get downside exposure to the space rather than just single stocks, so it is interesting to read that Tuttle Capital plans to launch the Short De-SPAC ETF today. The ETF aims to make money on the stock losses of the 25 largest firms that have merged with special purpose acquisition companies. That includes once-hot stocks like Clover Health, Lordstown Motors and QuantumScape who have all sold off sharply this year (see below). The Short De-SPAC ETF will use derivatives contracts, also known as swaps, to deliver the inverse return of the De-SPAC index. The index is rebalanced monthly. It is worth noting that because shorting SPACs even with swaps is difficult, the ETF may not track the index perfectly.

Oxford/AstraZeneca booster works well, study finds

Some good news to brighten up your Wednesday. A study has found that the Oxford/AstraZeneca Covid-19 vaccineworks well as a third booster shot, despite concern that the immune system might fight off the adenovirus used as a delivery mechanism. A third dose was shown to boost participants’ antibodies to the coronavirus’s spike protein in an upcoming study by Oxford university, according to people familiar with the matter. The study strengthens the case for using the AstraZeneca vaccine as a booster shot if the immunity in participants begins to wane over time, or if it would help the body fight new variants of the virus behind Covid-19. One interesting angle that is often overlooked is that this could actually be meaningful for AstraZeneca in the medium-term. While the company is providing the vaccine at cost (well Q1 was at a loss actually), once the pandemic is ‘over’ they may be able to start charging for the vaccine and as a result, booster shots could be sold on an annual market that analysts estimated last year could be worth about $10bn.