Companies at risk ahead of earnings | Uber goes German | ESG coming to America | Virus resurgence?

Your Daily KnowHow

In today’s KnowHow…

Which companies are at risk during earnings?

Uber – Zeit zu liefern…

ESG is coming to the US in a big way

Inflation risks higher, coronavirus resurgence main risk

What happened overnight…

We spoke on Monday about whether the punches Biden was throwing at the Tobacco names would lead to a refocussing from investors on other areas of Biden’s campaign plans. We are seeing this play out today with clean energy names outperforming throughout Europe as investors eagerly await the two-day global climate change conference that Joe is holding today and tomorrow. Outside that, strong results from Nestle and Volvo have further supported the European market. US futures are mixed as investors weighed reflation bets (more below) against the outlook for earnings (more below) and a resurgence in global virus cases. Treasuries remained steady at 5-week lows. Intel and SNAP results will be a key focus for investors in the US today.

Chart of the Day

Clubhouse’s monthly installs have been falling dramatically since launch. Cause for concern? Possibly. Competition is ramping up. The team at KnowHow enjoy our Twitter Spaces tune-ins and Facebook is set to launch it’s own me-too product. Is Clubhouse a goner then? Not necessarily, even if new installs are falling, if churn remains low, that’s still a pretty captive and potentially profitable customer.

Analysis

Which companies are at risk during earnings?

Thinking bigger picture about this earnings season, there’s two clear lessons we should take from Netflix’s earnings on Tuesday night:

risk of pulled forward demand in 2020

getting a handle on expectations

The first point will clearly be tough through the next couple of reporting periods particularly for many of the early pandemic winners. As Netflix showed below, companies are struggling to forecast themselves internally, so what hope do sell-side analysts have.

The second point follows on from the first in many ways. Getting a handle on expectations is tough particularly given the volatility in demand and difficulty in forecasting at the moment. However, one way we think is always helpful is to look at the relationship between recent share price moves relative to sell-side earnings expectations. It is certainly not fool proof. BUT, i) the share price move going into earnings gives you a sense of expectations and, ii) comparing that with recent changes in earnings estimates gives you insights on what sell-side analysts are expecting from speaking to the company or any proprietary modelling data they may have.

The chart below is for companies reporting until 30th April.

Naturally, companies in the bottom-right quadrant should raise some concern and likewise, companies in the top-left are potentially set-up well. FYI… this was the analysis we did last week when we suggested that Pinterest, a stock we like a lot, may be running too hard into earnings. Netflix would also have shown up on that list in hindsight. Last week’s pull back has now improved the Pinterest set-up pre earnings considerably.

So, lets get into it…

Which stocks are at risk ahead of earnings next week and which could be potential opportunities?

On the whole, we have seen a healthy flush out in many growth names over the past week which suggests risks are now far more balanced. Microsoft is the name that looks most exposed in our view as investors chase Azure growth expectations.

On the more attractive side, Discovery certainly looks interesting post the Archegos sell down. And, we would also highlight Spotify where analysts have gradually been raising estimates despite the shares remaining choppy.

Uber – Zeit zu liefern…

Our regular readers will know we are big fans of Uber. We initially wrote on the company at the end of March with the key driver of our thesis pointing to Uber Eats and how the true value is under-appreciated. Post the news of their entrance into Germany we thought we would update our thinking and why we still continue to like the stock.

What is new?

The FT reported yesterday that Uber is attempting to break what it called Just Eat Takeaway.com’s “monopolistic” stranglehold on the German food delivery market starting in Berlin in the next few weeks. To quote Pierre-Dimitri Gore-Coty, Uber’s senior vice-president of delivery, in Germany “you have one player that is effectively dominating that country”, describing Just Eat Takeaway’s commission rates as “extraordinarily high”. Uber Eats’ expansion into its largest untapped takeaway market in Europe follows a period of retrenchment. Last year it exited India and several smaller markets in eastern Europe, Latin America, the Middle East and Africa, after leaving South Korea in late 2019.

Why we like it:

We view this as a timely challenge to a monopoly in a market that can easily hold more than one competitor. The company has already signed up ‘dozens’ or restaurants that include household chains and to quote Gore-Coty: “If I judge by the experience we have in places like Spain or even in smaller countries like Netherlands or Belgium [where Just Eat Takeaway also dominates], I’m pretty convinced that this will translate into actually very rapid growth for Uber.” We think the best way to highlight the opportunity for Uber is to use the chart below.

We note that breaking into a new market is still very difficult and we do not factor in any success in the market at the moment but Just Eat Takeaway’s approach to delivery in Germany has in our view exposed the company to competitors and this will likely lead to high growth in Germany for the company.

Mobility update

In our original analysis we also focussed on how mobility will driver Uber’s recovery in the rides side of the business. We have updated the below chart and as you can see, while parts of Europe are still taking a while to recover, the UK and USE have shown marked improvements over the last month. We foresee a situation in Q2 where mobility improves substantially but delivery remains very high as restaurants and bars access continues to be restricted. For us, this goldilocks situation is hugely supportive for Uber.

Mobility Trends – DM Countries

Conclusion

We like the expansion; we like the market, and we see mobility increasing supportive for the Uber share price. This is a stock that remains a key own for us with 40% upside in the near-term and EV / Autonomous optionality driving the next leg of the story.

What we’re reading

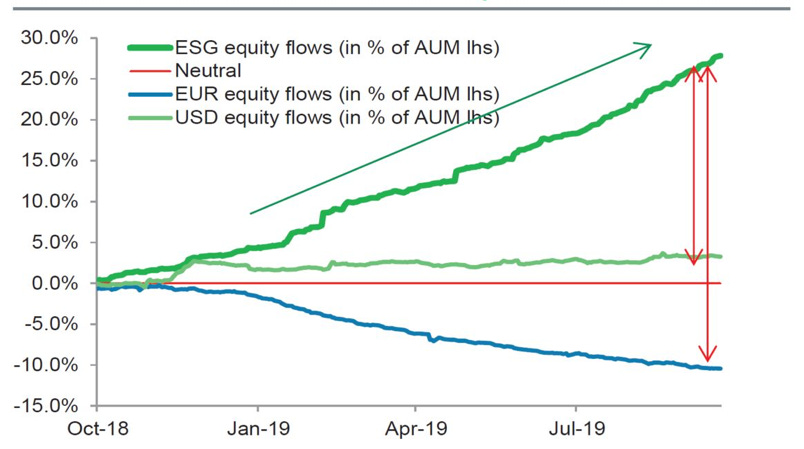

ESG is coming to the US in a big way

This is a big year for climate change and it kicks off with today’s summit of 40 world leaders. The US will announce plans to reduce its carbon emissions by up to 50% versus 2005 levels by 2030 according to most reports. To give you some context, Obama’s original target was 26-28% by 2025. This is a step-up. Plus, we already know the heavy focus on green investments in the America Jobs Plan.

But, from an investing perspective, it’s worth paying particularly attention to Treasury Secretary, Janet Yellen’s speech to the Institute of International Finance yesterday. Reporting and reliability of climate/environmental data is challenging both to grasp the potential climate impact of a business’ actions but also to assess the impact to the business of climate related risks/natural disasters. In Europe, significant progress has been made on this through the years and ESG funds have been a game-changer for active fund managers. The performance of ESG stocks have also followed. Have a look at this chart from Bloomberg’s Quint from a year ago.

This is now coming to the US in a big way and is a major focus for the Treasury to direct capital towards climate winners. Key bit from Janet Yellen’s speech below.

“the SEC is currently reviewing its 2010 guidance on climate-related disclosures. Treasury will work with the SEC as part of its participation in international discussions to promote effective and consistent approaches to disclosure. We are closely following progress of and support the International Financial Reporting Standards Foundation establishing a Sustainability Standards Board that will focus first on developing a climate disclosure standard”

Inflation risks higher, coronavirus resurgence main risk

It is somewhat alarming the number of scientists, politicians and economists that are starting to flag the risk of another coronavirus resurgence. Britain’s PM Boris Johnson, who started off the latest re-opening with a view that there would be no need for another lockdown post vaccinations, is now merely “hopeful” that another lockdown is not needed. This latest Reuters poll of economists over the last week suggests 70% now see a resurgence of coronavirus as the biggest risk to the US economy over the next three months. In reality, that’s probably too alarmist but as we highlighted in our Chart of the Day yesterday, cases continue to rise in countries receiving the Sinovac vaccine and, variants as we are seeing in India remain a major risk. We fully expect politicians to go hard on International travel to avoid any issues.